Homes and Condos for Sale and Rent in Miami

Integrated Services 360° 360°

Acquire the Perfect Property

Find the perfect property in Miami and buy high-quality new and used real estate. Our real estate agents have extensive experience and knowledge to provide you with the specialized advice you need.

Customized Financing Solutions

Purchasing a property often requires solid financing tailored to the buyer's financial capacity. That's why we offer flexible and personalized mortgage loans for foreigners with a minimum of 30% down payment. We tailor the conditions to your needs.

Generate Extra Income through Renting

We provide comprehensive assistance to transform your real property into a source of dollar income, managing all stages of the rental to maximize optimal return on investment.

Property Management

We have a team ready for the professional care and preventive and corrective maintenance of your home. We optimize costs and benefits to ensure efficient management of your real estate investment.

Comprehensive Legal and Accounting Advisory

Our interdisciplinary team of real estate professionals provides expert advice to clarify any doubts about accounting and legal services involved in buying, selling, and renting real estate. We ensure regulatory compliance with the Fair Housing Act.

Our apartments portfolio

Our houses portfolio

Projects in Orlando

Find your property in Miami

We have a wide portfolio of properties that are perfect for you

Aventura

Aventura Bal Harbour

Bal Harbour Bay Harbor Islands

Bay Harbor Islands Boca Raton

Boca Raton Coconut Grove

Coconut Grove Coral Gables

Coral Gables Dania Beach

Dania Beach Davie

Davie Doral

Doral Fort Lauderdale

Fort Lauderdale Hallandale Beach

Hallandale Beach Hollywood

Hollywood Homestead

Homestead Kendall

Kendall Golden Beach

Golden Beach Key Biscayne

Key Biscayne Miami Beach

Miami Beach Miramar

Miramar Palm Beach

Palm Beach Palmetto Bay

Palmetto Bay Pembroke Pines

Pembroke Pines Pinecrest

Pinecrest Pompano Beach

Pompano Beach Sunny Isles Beach

Sunny Isles Beach West Palm Beach

West Palm Beach Weston

Weston Wilton Manors

Wilton Manors

2,000 clients from around the world have invested in Miami thanks to PFS

22 years of experience in property sales in the United States

Our long-standing track record as leaders in the Miami real estate market positions us as your best choice. We have a proven track record that backs our reliable service and successful results.

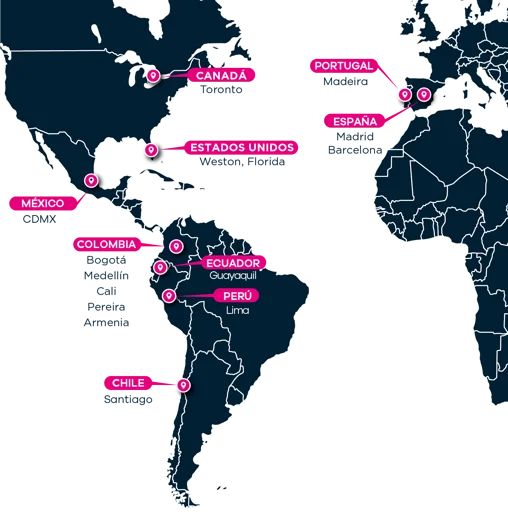

65 advisors in 12 countries in the Americas and Europe

A wide network of 65 advisors strategically located in the Americas and Europe to maximize your real estate investment opportunities.

More than 2,000 satisfied customers trust us

With an international network of agents, we offer global and localized perspectives that enhance our ability to find unmatched opportunities. From advice to closing the deal, we optimize your real estate investment opportunities.

Testimonials

Arturo Calle“Que personas, que organización, saben vender el producto y tienen un concepto de honestidad y honradez que felicito desde todo punto de vista”Colombia

Arturo Calle“Que personas, que organización, saben vender el producto y tienen un concepto de honestidad y honradez que felicito desde todo punto de vista”Colombia César Augusto Londoño“Fue realmente maravilloso, el conocimiento de Patricia es excepcional, lo que Gustavo sabe del negocio es fabuloso…quedé absolutamente encantado y emocionado.”Colombia

César Augusto Londoño“Fue realmente maravilloso, el conocimiento de Patricia es excepcional, lo que Gustavo sabe del negocio es fabuloso…quedé absolutamente encantado y emocionado.”Colombia Javier Aparicio“Decidí invertir con ustedes, y ahora digo que fue el gran acierto de mi vida”Mexico

Javier Aparicio“Decidí invertir con ustedes, y ahora digo que fue el gran acierto de mi vida”Mexico